For budget-conscious individuals, a health cash plan is not just insurance—it’s a financial strategy that makes routine healthcare costs profitable.

- It systematically outperforms a standard savings account for predictable expenses like dental check-ups and eye tests.

- Success hinges on strategic use: mastering receipt requirements and timing treatments to maximize annual allowances.

Recommendation: Use the self-assessment in this guide to determine if a cash plan strategy aligns with your personal dental and health risk profile.

For many in the UK, routine healthcare costs are a frustrating reality. The annual dental check-up, the new pair of glasses, the series of physiotherapy sessions—these are predictable expenses that NHS services don’t always cover in full. The common response is to either begrudgingly pay out-of-pocket, depleting savings, or to assume the only alternative is a comprehensive and costly Private Medical Insurance (PMI) policy. This leaves a significant gap for those who are budget-conscious but still want to manage their health proactively.

While many have heard of health cash plans, they are often misunderstood as just another form of insurance. This view misses the core value proposition. The key is to stop thinking of them as a safety net and start seeing them as an active financial tool. When used correctly, a cash plan offers a form of financial arbitrage: you pay a small, fixed monthly fee to unlock a much larger pot of money for expenses you were going to incur anyway. It’s a system designed to give you a positive return on your predictable healthcare spending.

This guide moves beyond the basics. We won’t just list benefits; we will deconstruct the strategies that turn a £15 monthly premium into over £300 of real-world value. We will cover how to ensure your claims are paid in hours, not weeks, the critical receipt error that leads to rejection, and how to strategically time your appointments to maximize every penny of your annual allowance. This is your playbook for making routine healthcare not just affordable, but financially advantageous.

This article provides a complete breakdown of how to leverage health cash plans to your financial advantage. Below is a summary of the key strategies and comparisons we will explore to help you take control of your routine medical spending.

Summary: Why Health Cash Plans Are the Best Way to Reclaim Routine Medical Costs?

- Why Paying £15 a Month for a Cash Plan Saves You £300 a Year?

- How to Claim 100% of Your Optical Fees Back within 48 Hours?

- Westfield or Simplyhealth: Which Cash Plan Offers Better Therapy Cover?

- The Receipt Error That Blocks 20% of Cash Plan Claims

- When to Visit the Dentist to Maximize Your Annual Cash Plan Allowance?

- Denplan vs Insurance: Which Option Save More on Regular Check-Ups?

- £1,000 Limit vs Full Outpatient Cover: Which Fits an Active Lifestyle?

- Is Private Dental Insurance Worth It for NHS Patients?

Why Paying £15 a Month for a Cash Plan Saves You £300 a Year?

The fundamental value of a health cash plan lies in a simple financial principle: leverage. You are not simply saving money; you are using a small, consistent payment to access a much larger pool of funds for predictable costs. For a budget-conscious individual, this is a more efficient use of capital than a traditional savings account, especially when dealing with routine medical bills that can easily derail a monthly budget. The average person’s annual healthcare spending provides a clear backdrop for why this matters.

Putting aside £15 a month into a savings account yields exactly £180 a year. If you then face a £150 bill for new glasses and two £60 dental check-ups, your savings are wiped out, and you’re still £135 out of pocket. A cash plan transforms this equation. That same £180 annual premium can unlock benefits worth £300, £400, or more. You claim back the cost of the glasses and the check-ups, and your personal savings remain untouched for genuine emergencies or other goals. This is the difference between passive saving and active financial management of your health expenses.

The comparison below starkly illustrates this. For predictable, recurring costs, a cash plan doesn’t just help you pay the bill; it generates a positive financial return on your premium, making it a superior tool for managing everyday health spending.

This direct comparison, based on a typical user scenario, shows how a cash plan can provide significantly more value than simply setting money aside, as detailed in an analysis by MoneySavingExpert.

| Scenario | £15/month Cash Plan (£180/year) | £15/month Savings Account (£180/year) |

|---|---|---|

| Annual eye test (£25) + glasses (£150) | Claim back £150-£200 depending on plan level | Withdraw £175, depleting savings |

| 2 dental check-ups (£60 each) | Claim back £100-£120 | Withdraw £120, further depleting savings |

| Total value after claims | £250-£320 in benefits received | £0 remaining in savings (£295 withdrawn) |

| Net benefit/loss | +£70 to +£140 gain | -£115 (spent more than saved) |

How to Claim 100% of Your Optical Fees Back within 48 Hours?

A key advantage of modern health cash plans is “benefit velocity”—the speed at which you can get your money back in your account. For someone managing a tight budget, waiting weeks for a reimbursement cheque is a significant drawback. Providers like Westfield Health have built their reputation on processing claims within 48 hours, but this speed is entirely dependent on one factor: the quality of your submitted receipt. A clean, detailed receipt is the passport to a fast, successful claim.

The single biggest mistake users make is assuming any proof of payment will suffice. It won’t. Insurers aren’t just verifying that you spent money; they are verifying that you spent it on a specific, covered treatment from a qualified professional. This is why mastering “receipt hygiene” is non-negotiable. It’s a simple discipline that dramatically increases your chances of a swift, no-questions-asked payout. In fact, industry data shows that a 95% acceptance rate is common for correctly presented claims, highlighting that failure is almost always due to avoidable administrative errors.

Before you even leave the optician’s practice, you must ensure your receipt is “claim-ready”. This means asking a few specific questions to get the right documentation from the start. The process is made even easier with mobile apps that allow you to simply photograph and upload the receipt instantly.

This visual represents the final, simple step of the claim process. However, the success of this step is determined by the preparation done beforehand. To ensure your submission is flawless, internalize the following checklist and make it a habit for every healthcare visit. Think of it as a pre-flight check for your claim.

- Question 1: ‘Can you provide an itemized receipt showing each service separately?’ – Ensure the receipt lists ‘Eye test: £X’ and ‘Prescription glasses: £Y’ rather than just a total amount.

- Question 2: ‘Is your professional registration number included on this receipt?’ – Confirm the optician’s GOC (General Optical Council) number appears on the document for insurer validation.

- Question 3: ‘Does this receipt show both the treatment date and payment date clearly?’ – Verify both dates are visible, as insurers use the treatment date to track your annual benefit allowance period.

Westfield or Simplyhealth: Which Cash Plan Offers Better Therapy Cover?

When it comes to therapy benefits—such as physiotherapy, acupuncture, or chiropractic services—the choice between major providers like Westfield Health and Simplyhealth isn’t just about the total annual limit. The structure of the coverage, the types of therapies included, and the speed of reimbursement can make a significant difference, especially for someone relying on these services for ongoing well-being or recovery.

Westfield Health often appeals to users who want flexibility, typically offering a combined pot of money that can be used across a range of different therapies. This is ideal if you’re not sure whether you’ll need physiotherapy or osteopathy during the year. Simplyhealth, on the other hand, often provides a more tiered structure, with specific limits that increase with the plan level. Both require practitioners to be registered with recognized professional bodies, a crucial check for claim validation.

However, a feature that often gets overlooked in comparisons is the claim processing time. As seen in the case study below, for a user undergoing an intensive course of therapy, getting reimbursed in 48 hours versus several weeks can have a huge impact on personal cash flow and the ability to continue treatment without interruption.

Cost-Benefit Analysis: 8 Psychotherapy Sessions

A user requiring 8 sessions of psychotherapy at £70 per session (total cost: £560) found that while the annual limits on mid-tier plans from both Westfield and Simplyhealth were comparable (covering around £350-£400), a key differentiator emerged. The ability to claim online and receive funds within 48 hours from Westfield was crucial. This rapid reimbursement meant they could pay for the next session without being significantly out of pocket, making the intensive therapy period financially manageable. This illustrates how “benefit velocity” can be as valuable as the benefit amount itself.

The following table, based on information from sources like specialist broker MyTribe Insurance, breaks down the key structural differences to help you decide which provider’s approach best aligns with your potential therapy needs.

| Feature | Westfield Health (Good4you) | Simplyhealth (1-2-3 Health Plan) |

|---|---|---|

| Therapy types covered | Physiotherapy, Acupuncture, Chiropractic, Osteopathy, Homeopathy | Physiotherapy, Osteopathy, Chiropractic, Acupuncture |

| Annual limit structure | Combined annual pot for all therapies (varies by level) | Tiered annual limits by plan level (Levels 1-6) |

| Claim processing speed | Within 48 hours for online claims | Standard processing times vary |

| Practitioner requirements | Must be registered with approved professional body | Must be certified by recognized associations (e.g., BACP, UKCP for counseling) |

| Additional mental health support | 24/7 counseling helpline included | Included on higher tiers |

The Receipt Error That Blocks 20% of Cash Plan Claims

There is nothing more frustrating than paying your premiums diligently, only to have a legitimate claim rejected. While it can feel arbitrary, the reality is that a significant percentage of rejections are not due to the treatment being uncovered, but due to simple, avoidable errors on the submitted paperwork. As regulatory findings from the FCA indicate, poor communication and lack of clarity are frequent culprits in claims disputes. For cash plans, this “lack of clarity” almost always points to one thing: the receipt.

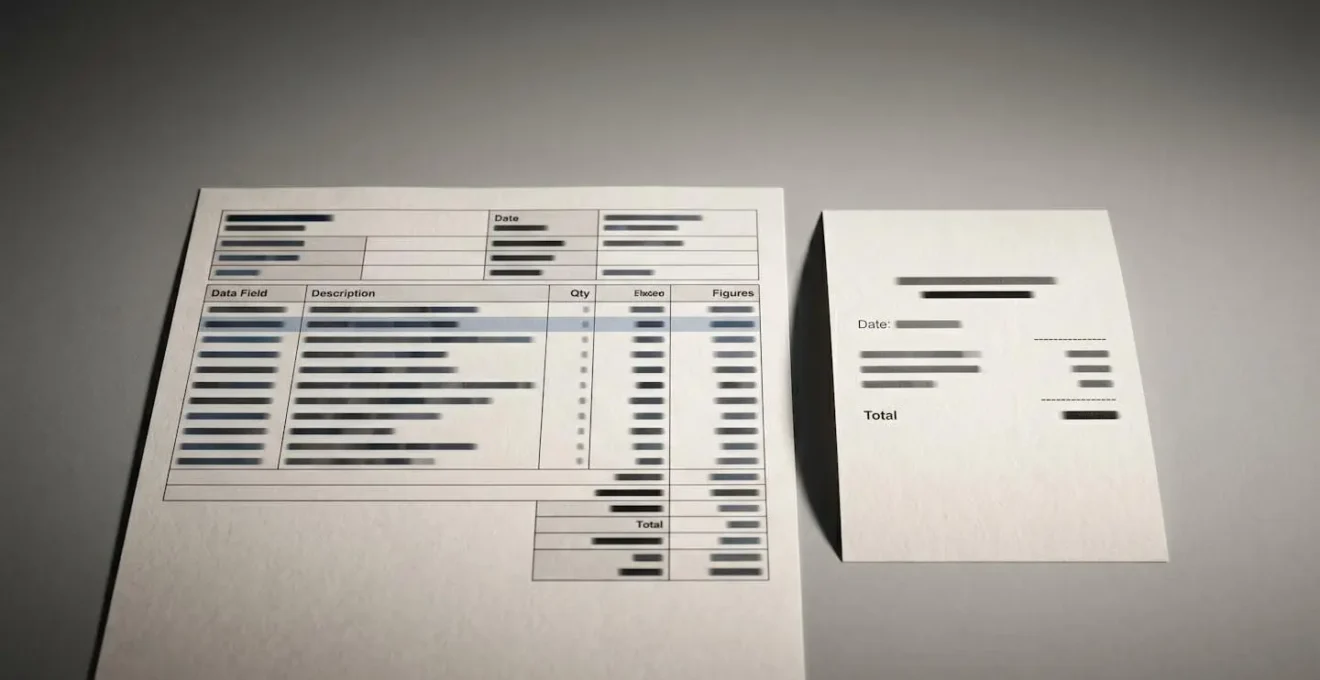

The core issue is a misunderstanding between a “proof of payment” and a “claimable receipt”. A debit card slip is a proof of payment; it shows you paid a certain amount of money. A claimable receipt, however, is a detailed invoice that tells the insurer a story: what specific treatment you received, when you received it, and who provided it. Without this information, the insurer cannot validate that the expense is covered under the terms of your policy. It’s the difference between a vague note and a detailed report.

This image below perfectly illustrates the problem. On the right, a simple card slip—useless for a claim. On the left, an itemized invoice—the key to getting your money back. Understanding this distinction is the first and most important step in mastering “receipt hygiene”.

Insurers’ automated systems are designed to flag receipts that lack essential information. To avoid triggering an automatic rejection, you must ensure your receipt is free of these three fatal flaws. Committing any one of them will almost certainly result in a delayed or denied claim, undermining the entire purpose of having a cash plan.

- Error 1 – Missing Itemization: Submitting a receipt showing only ‘Total: £125’ instead of an itemized breakdown (‘Dental Check-up: £60’, ‘Scale & Polish: £65’). Insurers require itemization to verify each service is covered under your plan category.

- Error 2 – Absent Practitioner Registration Number: Missing the dentist’s GDC (General Dental Council) or optician’s GOC (General Optical Council) registration number. Insurers use this for fraud prevention and to confirm the practitioner is qualified and authorized.

- Error 3 – Debit Card Receipt Only: Submitting a card machine slip without the official practice receipt. Card receipts lack treatment details, practitioner information, and itemization required for claim validation.

When to Visit the Dentist to Maximize Your Annual Cash Plan Allowance?

For a truly savvy cash plan user, maximizing value goes beyond simply submitting claims. It involves strategic planning of treatments to make the most of your annual benefit limits. This concept, which can be termed “allowance optimization,” is particularly powerful when it comes to high-cost dental work. Most people assume their benefit year aligns with the calendar year, but it usually resets 12 months from the date of your *first claim*. Understanding and using this timeline is key.

There are two primary strategies for timing your claims: front-loading and back-loading. Front-loading involves claiming for routine, low-cost care like check-ups early in the policy year. This guarantees you get some value back from your premiums. Back-loading means preserving your allowance for potential emergencies or more significant treatments later in the year. A hybrid approach is often best: use it for small, predictable costs early on, but keep the bulk of your high-value dental or optical allowance in reserve.

The most advanced strategy, however, comes into play when you know you need a multi-stage, expensive treatment that exceeds your annual limit. By strategically splitting the treatment across two benefit years, you can effectively claim against your allowance twice for a single course of treatment, as the following case study demonstrates.

The Benefit Year Reset Strategy

A Westfield Health member required a root canal with a total cost of £800. Their annual dental limit was £400. Instead of doing the whole treatment in one benefit period and being £400 out of pocket, they used a clever timing strategy. They scheduled the initial consultation and first stage of treatment in November, near the end of their benefit year, claiming the first £400. Then, they scheduled the completion of the treatment in January of the following year. This allowed them to claim another £400 from their newly reset allowance, as confirmed by details on the provider’s site. Their total out-of-pocket cost for the £800 procedure was zero. This is the pinnacle of allowance optimization.

This level of planning transforms a cash plan from a simple reimbursement service into a powerful financial tool for managing significant healthcare costs. It requires foresight but can save you hundreds of pounds on necessary treatments.

Denplan vs Insurance: Which Option Save More on Regular Check-Ups?

When considering private dental care, the choice often comes down to two models: dental insurance (like that offered by a cash plan) or a capitation plan (with Denplan being the most well-known brand). They might seem similar, but they operate on fundamentally different principles, and the best choice depends entirely on your relationship with your dentist and your preference for payment models.

Dental insurance, or the dental portion of a health cash plan, is a reimbursement model. You visit any private dentist, pay for your treatment upfront, and then claim a percentage of the cost back from the insurer, up to your annual limit. This offers flexibility in your choice of dentist but requires you to manage the claims process and handle the initial cash outlay.

Denplan, on the other hand, is a subscription model. You pay a fixed monthly fee directly to a specific dental practice. In return, all your routine care—such as check-ups, hygiene visits, and X-rays—is covered. You don’t pay at the time of the visit and there are no claims to file. This provides budget predictability but ties you to a single practice. With industry data revealing that around half of all UK dental practices are Denplan members, it’s a widely available option. For restorative work, Denplan usually offers a discount, whereas a cash plan would reimburse a portion of the cost.

The choice boils down to what you value more: the flexibility to see any dentist (cash plan) or the convenience and budget predictability of an all-in-one subscription with your chosen dentist (Denplan).

| Feature | Denplan Essentials (Capitation) | Dental Insurance (Cash Plan) |

|---|---|---|

| Average monthly cost | £13-£22 per month | £11+ per month for basic plans |

| Annual cost range | £156-£264 | £132+ depending on level |

| What’s included in routine care | Check-ups, hygiene visits, X-rays, 10% discount on restorative work | Claim back costs up to annual limits for check-ups and treatments |

| Payment model | Subscription directly to your dentist (predictable, all-inclusive) | Claim reimbursement model (pay first, claim later) |

| Restorative work (fillings, crowns) | 10% discount; higher tiers may include some restorative work | Partial reimbursement up to annual limits |

| Dentist flexibility | Tied to specific Denplan-registered practice | Usually any dentist, then claim back |

Key Takeaways

- Health cash plans offer financial arbitrage, turning small monthly fees into larger benefits for predictable costs like dental and optical care.

- Claim success and speed depend on “receipt hygiene”—itemized receipts with practitioner registration details are non-negotiable.

- Strategic timing of treatments, such as splitting them across benefit years, can effectively double your coverage for major procedures.

£1,000 Limit vs Full Outpatient Cover: Which Fits an Active Lifestyle?

For individuals with an active lifestyle—runners, team sports players, or regular gym-goers—the risk of injury introduces a new dimension to health coverage. The question is no longer just about routine care but about managing injuries. This is where the distinction between a health cash plan and a full outpatient Private Medical Insurance (PMI) policy becomes critical. They are designed for two different types of problems: predictable maintenance versus unexpected events.

A health cash plan, with a typical therapy limit of around £1,000, is perfectly suited for managing chronic or repetitive strain injuries. Think of a runner who needs regular physiotherapy to manage knee pain. The cash plan excels here, covering a predictable number of sessions throughout the year without a large upfront cost. It’s a tool for maintenance and ongoing care.

Full outpatient PMI, however, is designed for acute, unexpected injuries. If a footballer tears a ligament and needs an immediate MRI scan to diagnose the damage, the outpatient cover is invaluable. It provides rapid access to expensive diagnostic tests and specialist consultations that a cash plan would not cover. The trade-off is a significantly higher premium and usually an excess to pay. The best strategy for some may even be a combination of the two.

Complementary Coverage for a Team Sports Athlete

A recreational rugby player demonstrated a savvy hybrid approach. They held a mid-tier cash plan (£15/month) for routine physio and a basic outpatient PMI policy (£40/month, £250 excess). After a shoulder injury, they used the PMI for a quick MRI scan, paying the £250 excess. The diagnosis required 10 physio sessions costing £600. Their cash plan then reimbursed £500 of this. Their total out-of-pocket cost was £350 (£250 excess + £100 uncovered physio) for treatment valued at £1,000. This dual-coverage strategy gave them the best of both worlds: diagnostic speed and affordable ongoing treatment.

The table below breaks down which type of cover is generally better suited for different scenarios common to an active lifestyle.

| Scenario | Cash Plan (£1,000 limit) | Full Outpatient PMI |

|---|---|---|

| Chronic/Repetitive Strain (Runner with ongoing knee issues) | BETTER: Covers regular physiotherapy sessions (10-15 sessions/year within £1,000 limit) | Limited: May only cover initial diagnosis; ongoing maintenance not typically covered |

| Acute Injury (Team sports player needing MRI + treatment) | Limited: Won’t cover expensive diagnostic scans (MRI £300-£500) | BETTER: Fast access to MRI, CT scans, specialist consultations |

| Annual cost comparison | £180-£300/year depending on plan level | £500-£1,200/year depending on age and excess level |

| Best suited for | Routine maintenance, predictable therapy needs | Unexpected injuries requiring immediate diagnosis |

Is Private Dental Insurance Worth It for NHS Patients?

For many NHS patients, the question of whether to take out private dental insurance or a cash plan can be perplexing. If you have access to an NHS dentist, why pay extra? The answer lies in the gap between what the NHS provides and what patients may want or need, particularly concerning restorative work, cosmetic options, and the sheer waiting times for non-emergency treatment. A cash plan acts as a bridge, making private options more accessible without requiring a full commitment to expensive private insurance.

The NHS provides excellent functional dental care, but its scope is limited. For example, crowns on back teeth are typically made of metal amalgam, not tooth-coloured ceramic. White fillings may only be offered on front teeth. If you require or prefer these more aesthetic options, you’ll have to pay for them privately. A cash plan can help you reclaim a significant portion of these private treatment costs, making the upgrade more affordable. It’s not about replacing the NHS; it’s about supplementing it strategically.

The decision ultimately comes down to your personal risk profile and priorities. Do you have a history of dental problems? Do you value cosmetic appearance? Are you involved in activities that increase your risk of dental injury? Answering these questions honestly can help you determine whether relying solely on the NHS is sufficient, or if the small monthly cost of a cash plan represents a smart investment in your future dental health.

Your Action Plan: Risk Profile Self-Assessment

- Factor 1 – Dental History: Do you have multiple existing fillings or crowns? If yes (+2 points), you’re at higher risk of needing restorative work. If no (0 points), NHS-only may suffice.

- Factor 2 – Age & Family History: Are you over 40 or do you have a family history of gum disease? If yes (+2 points), preventative private care becomes more valuable. Under 30 with good family history (0 points).

- Factor 3 – Lifestyle Factors: Do you play contact sports, grind your teeth, or consume acidic foods regularly? If yes (+2 points), your risk of dental damage increases. If no (0 points).

- Factor 4 – Cosmetic Priority: Do you value white fillings on back teeth or premium crown materials not covered by the NHS? If yes (+1 point). If no (0 points).

- Review Your Score: A score of 0-2 points suggests NHS plus a savings account is likely cost-effective. A score of 3-5 points indicates a cash plan is highly recommended. A score of 6-7 points justifies considering full private dental insurance or a comprehensive Denplan scheme.

Stop letting routine medical bills be a random drain on your finances. By applying these strategies, you can transform them into a predictable and managed part of your budget. The first step is to use this assessment to understand your own needs and determine if a health cash plan is the right financial tool for you.